Published below is the conclusi on of a three-part report delivered on January 22, by Nick Beams to an expanded meeting of the World Socialist Web Site International Editorial Board (IEB). Beams is a member of the WSWS IEB and National Secretary of the Socialist Equality Party (Australia), which hosted the meeting in Sydney from January 22 to 27, 2006. Part one and Part two were published on February 28 and March 1, respectively. David North’s opening report to the WSWS IEB meeting was published on 27 February. Further reports will be published subsequently.

To conclude this survey, let me cite recent remarks by the Bank of England’s deputy governor for financial stability, Sir Andrew Large. Large pointed to what he called “some less benign aspects” of the present-day financial system, including the difficulty of knowing the real value of assets and contracts, a reliance on financial models that have not been tested over a range of economic conditions, uncertainty about the behaviour of new participants in the market and “the difficulty we have in judging just how deep markets will prove to be should a number of substantial investors decide simultaneously to try to realise their investments. ... The question is: are vulnerabilities mounting, and will they one day crystallise when a bigger shock arrives that the market simply cannot absorb? The fact is, we just don’t know.”

The growth of exotic financial instruments, many of which did not exist even a few years ago, is quite extraordinary. Hedge funds now have at their disposal at least $1 trillion, an amount which has doubled since 1998. And it is estimated that in 2006 the derivatives market will grow to half a quadrillion; that is, to $500 trillion, more than 10 times the world’s GDP—which is around $45 trillion.

Another significant event of the recent period has been the rise in the gold price, now hitting 25-year highs of around $560 per ounce. The shift into gold reflects the growing lack of confidence in all the major currencies. When the Nixon administration removed the gold backing from the US dollar in 1971, ending the Bretton Woods system, the dollar became an international fiat currency. But in the 35 years since, it has never been able to provide a stable basis for the international monetary system.

In the period of stagflation at the end of the 1970s, the dollar dropped to record lows, leading eventually to the Volcker shock in 1979, when US interest rates were lifted to record levels. This resulted in the deepest recession since the 1930s and a major financial crisis in the so-called under-developed countries. The increase in the value of the US dollar led to a widening trade gap, as US exports were priced out of world markets. This resulted, in 1985, in the Plaza agreement, under which the central banks agreed to lower the dollar’s value. But that decision had far-reaching consequences, not the least of which was an increase in the value of the yen and the creation of an assets and stock market boom in Japan that eventually collapsed in 1989, giving way to more than a decade of deflation.

The dollar had fallen so rapidly that by 1987 there was agreement that its value had to be stabilised—resulting in the Louvre agreement. However, differences between the US and Germany over interest rates led to turbulence in financial markets and the share market crash of October 1987.

The newly installed Federal Reserve Board chairman Alan Greenspan responded to the crash in a way that was to become very familiar over the next 18 years. He opened up the financial spigots, guaranteeing credit to financial institutions that might experience difficulty. The share market collapse was thus halted—with massive intervention by financial authorities—but the currency storms continued. The early 1990s saw a crisis of the British pound and of the Scandinavian banking system. Then came the Mexican crisis of 1994, in which the Clinton administration intervened to bail out US banks and financial institutions.

By the end of 1996, it was apparent that a stock market bubble was developing in the United States—a fact that was acknowledged by Greenspan during a meeting of the Fed board. But apart from one statement about “irrational exuberance” no action was taken. Wall Street’s opposition to the one interest rate rise initiated by Greenspan in 1997 was so intense that the Fed chairman concluded that no action should be taken to halt the escalation of share prices. In any case, the eruption of the Asian crisis was the signal for an easing of liquidity.

When the share market bubble eventually burst in early 2001, Greenspan’s response was to cut interest rates. The effect was to create a housing market bubble as interest rates went to record lows. In the recent period, the Fed has lifted rates, largely out of fear that, unless it did so, it would have no response when the next financial crisis hit.

The contradictions of capitalism

No doubt when a financial crisis does develop, there will be many who will lay the blame at Greenspan’s door ... if only the Fed had acted to nip the financial bubble in the bud, etc. etc., in the same way that attempts have been made to blame the policies of the Fed for the Wall Street collapse in 1929 and the Great Depression that followed.

While it would be wrong to deny the significance of individuals and their decisions, the expansion of the financial and credit system, and the potential instability it introduces, cannot be put down to the decisions of Greenspan. His policies were a response to the development of objective contradictions within the capitalist economy itself.

How do we assess these processes?

In the early 1970s, the post-war equilibrium of world capitalism broke down. The next three decades saw a vast transformation in world economy. We now face the question: are we moving towards a new equilibrium, or have the deep-going changes in the world economy over the past three decades created the conditions for economic and political upheaval and the possibility for the overthrow of capitalism by means of the socialist revolution. What, in other words, are the world prospects for socialism?

In order to address this question, I would like to consider an article by “left” writers Leo Panitch and Sam Gindin entitled “Finance and the American Empire” published in the 2005 edition of the Socialist Register.

The theme of the article is that financialisation processes over the past 30 years have not weakened but strengthened American capitalism. According to the two authors, the Volcker shock of the early 1980s and the neo-liberal agenda that followed it have been pivotal in bolstering American imperialism.

“Ultimately,” they write, “the risks involved in international accumulation are contingent on the confidence in the dollar and its material foundations in the strength of the American economy, and in the capacity of the American state to manage the inevitable volatility of financial markets. The post-war boom had reflected a kind of confidence in American power; the reconstitution of empire that began in the early 1980s was about restoring it after the uncertainties of the 1960s and 1970s.”

They insist that the expansion of finance has been central to both the internationalisation of production and the continuing strength of the American economy; liberalised finance is a developing mechanism through which the American state addresses its goals, as well as managing financial crises as they arise. At the same time, the globalisation of finance has seen the Americanisation of finance, which has become central to the reproduction and universalisation of American power.

Panitch and Gindin dismiss what they call the “old paradigm of inter-imperialist rivalry” on the grounds that the current integration into the American empire means that a crisis of the dollar is a crisis of the system as a whole.

“Clinging to the notion that the crisis of the 1970s remains with us today flies in the face of the changes that have occurred since the early 1980s. What kind of crisis of capitalism is it when the system is spreading and deepening, including through sponsoring another technological revolution, while the opposition to it is unable after three decades to mount any effective challenge? If crisis becomes ‘the norm’, this trivializes the concept and diverts us from coming to grips with apprehending the new contradictions of the current conjuncture.”

A number of points need to be made here. Of course it is necessary to distinguish between a short-term crisis of the capitalist economy—the share market collapse of 1987, the collapse of Long Term Capital Management—and the long-term historical viability of the capitalist mode of production in the present epoch. Capitalism is not permanently in crisis in the short-term, nor should the “crisis of capitalism” be invoked to try to explain economic developments.

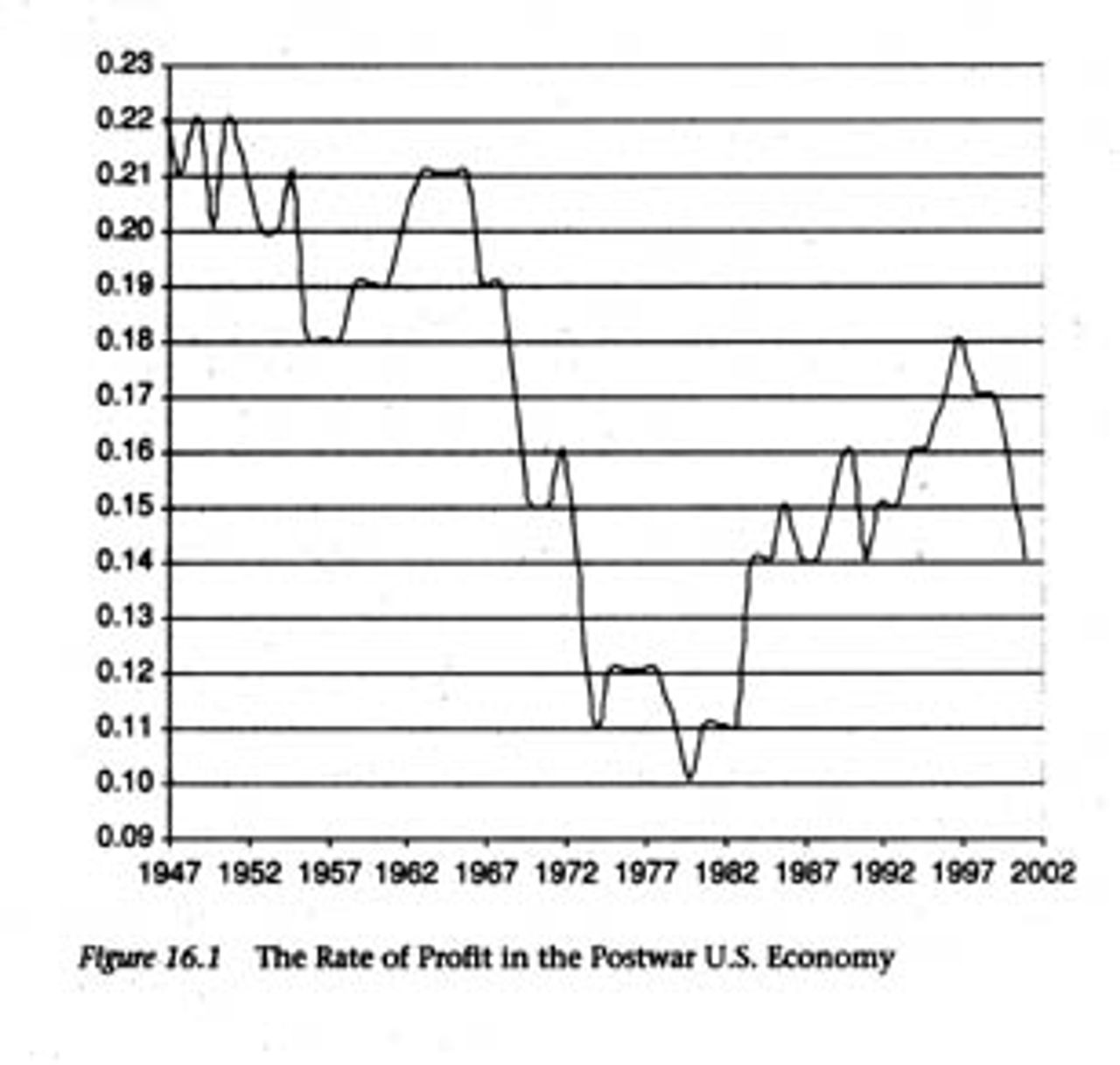

That having been said, it is necessary to make an assessment of the historical position of the world capitalist economy. What was the “crisis of the 1970s” which our two authors insist must now be discarded? It was rooted in the process of capital accumulation—the driving force of the capitalist economy. The tendency of the rate of profit to fall, which developed from the end of the 1960s, could not be overcome within the existing system of production. Capitalist economy needed a radical restructuring. This is what led to the process of globalisation—the attempt by capital to overcome the pressure on profit rates by taking advantage of the cheapest sources of labour. Has the rate of profit been restored? The evidence would suggest not.

According to one analysis, the US rate of profit stood at 22 percent at the start of the post-war boom, before undergoing a decline in the period from 1967 to 1977, when it stood at about 10 percent. Since then, despite the most strenuous efforts by both employers and the state to suppress real wages and to introduce new technologies, the rate of profit has risen to just 14 percent after a brief spurt in the 1990s. (See Fred Moseley, “Marxist Crisis Theory and the Postwar US Economy” in Anti-Capitalism Alfredo Saad-Filho ed. p. 212)

Even in the absence of specific figures, the emergence of a series of huge financial bubbles, in which wealth is gained not through the extraction of surplus value, but through speculation and financial means, points to the existence of downward pressure on profit rates. Money has to be made via financial ventures because it cannot be made anywhere else.

Panitch and Gindin insist that it is necessary to apprehend the “new contradictions of the currency conjuncture.” What are these? Inter-imperialist contradictions, they tell us, are a thing of the past and the falling rate of profit, which induced a crisis in the 1970s, is no longer with us. Accordingly, we must recognise the growing strength of US imperialism, and put away our old notions and perspectives based on an understanding of the objective contradictions of world capitalism. Does this mean socialism is ruled out? No, but it has a new foundation.

“A future beyond capitalism is possible, and increasingly necessary from the perspective of social justice and ecological sanity, but capitalism is still in the process of being made.” So we can still speak of the contradictions of capitalism, but we should not make too much of them, unless they take the form of class contradictions. We must “dispense with the notion of ‘crisis’ as something that leads capitalism to unravel on its own.”

“The openings for radical change [not, it should be noted, for socialist revolution] in the present era of capitalism will generally revolve around problems of political legitimacy rather than any sudden economic collapse.”

Here, in the first decade of the twenty-first century, are raised all the issues that erupted in the revisionist controversy at the beginning of the twentieth. As Rosa Luxemburg explained in her reply to Eduard Bernstein, either the socialist transformation of capitalism is the consequence of the international contradictions of capitalism and its eventual breakdown or the capitalist system is able to suppress its internal contradictions. “In that case socialism ceases to be a historic necessity. It then becomes anything you want to call it, but it is no longer the result of the material development of society.”

Bernstein had insisted that the new means of credit and finance had prevented the eruption of the type of crises that had shaken capitalism in the past and had strengthened the capitalist economy. Luxemburg replied that the credit mechanism, while overcoming contradictions in the development of capitalism, only did so by reproducing them at a higher level.

In words which have lost none of their relevance, she explained that “credit, instead of being an instrument for the suppression or attenuation of crises is, on the contrary, a particular mighty instrument for the formation of crises. It cannot be anything else. Credit eliminates the remaining rigidity of the capitalist relationship. It introduces everywhere the greatest elasticity possible. It renders all capitalist forces extensible, relative and mutually sensitive to the highest degree. Doing this, it facilitates and aggravates crises, which are nothing less than the periodic collisions of the contradictory forces of capitalist economy.”

While the central bankers cited earlier may not be students of Rosa Luxemburg, they were expressing their concerns over precisely this process.

The betrayals of the working class and the role of US imperialism

In conclusion, let us consider the assertion that the process of financialisation has strengthened the position of American capitalism, its dominance of the global capitalist system, and has given capitalism as a whole a new lease of life.

In reply, we must examine the historical relationship of America to the world capitalist system. On the eve of the Russian Revolution, Lenin spoke of imperialism as the latest phase of capitalism, as the eve of the socialist transformation. Trotsky’s perspective of permanent revolution was grounded on the understanding that while Russia, considered in isolation, was not ripe for socialism, the advanced capitalist economies certainly were. Therefore, the Russian Revolution could form the opening of the world socialist revolution.

In the event, the Bolsheviks’ revolutionary perspective was not realised and, in the course of the twentieth century, there was a further development of the productive forces under capitalism. As our authors remind us, there is, today, a technological revolution taking place. Should we perhaps conclude that the Russian Revolution was premature, that it was destined to be isolated, and that, therefore, the degeneration of the revolution, the rise of Stalinism and all that followed was inevitable?

This would be a completely mechanical approach. One only has to look at the tremendous costs to humanity associated with the continuation of the capitalist system in the twentieth century to answer that question.

The fact that the productive forces have continued to grow does not invalidate a revolutionary perspective on the grounds that capitalism had not completely exhausted itself. It does, however, help us to understand why such a perspective was not realised. The continuation of capitalism and the further development of the productive forces was made possible because of the enormous strength of American capitalism.

The International Committee has repeatedly emphasised the significance of the betrayals of the struggles of the working class by the Stalinist and reformist leaderships in the maintenance of capitalism in the twentieth century. It is necessary also to examine the interaction between these betrayals and the role of the United States.

The eruption of world war in 1914 signified the end of the organic peaceful development of capitalism and the opening of the epoch of social revolution. But the working class, except in Russia, was not able to overthrow the bourgeoisie. This was by no means a foregone conclusion. Not the least important factor in the decision by the United States to intervene in the war was the realisation that the longer it continued, the greater the danger of social revolution. Wilson’s famous 14 Points were drafted as an answer to the Bolshevik challenge and the threat posed by the Russian Revolution to the stability of the entire capitalist order. Had it not been for the American intervention, Germany would not have sued for peace and the European powers would have continued the war. Under those conditions, the war may well have been ended, not by American intervention, but by the social revolution.

The bourgeoisie was able to stabilise the situation, but it could not resolve any of the problems that led to the war. A series of potentially revolutionary situations developed in Germany in the early 1920s. That era was brought to a close when the unpreparedness of the German Communist Party resulted in the missed opportunity of October 1923. But even that would have been only an incident in an ongoing and deepening crisis, had not the US intervened with a plan for the restabilisation of Germany and Europe—the Dawes Plan.

It is important to stress, however, that, were it not for the betrayals of social democracy in the war, and in its immediate aftermath, American imperialism would not have been able to intervene.

In the political situation created by those betrayals, the strength of US capitalism was able, at least temporarily, to stabilise the situation. But it could not resolve the economic problems of world capitalism—they were to erupt just six years later in the Great Depression. Nevertheless, the temporary economic restabilisation had enormous political consequences in the continued isolation of the Soviet Union, the rise of the Stalinist bureaucracy, and the enormous damage this was to inflict on the newly established sections of the Communist International.

There is no question but that the Stalinist parties played the decisive political role in stabilising world capitalism in the aftermath of World War II. But without the ability of the US to lay the foundations for the growth of the international capitalist economy, the situation would have been very different. Under conditions of a deepening post-war economic crisis, the sections of the Fourth International would have been presented with the opportunity to challenge for leadership as the working class came into conflict with its Stalinist and reformist leaderships.

Instead, the stabilisation of world capitalism under the auspices of American imperialism saw the continued domination of these bureaucratic apparatuses over the working class and the isolation of the Fourth International, a process reflected in the development of various revisionist trends and currents.

In the aftermath of World War II, unlike the period following World War I, the US, resting upon the treachery of the Stalinist and social democratic leaderships, was able to establish a new capitalist equilibrium as the bearer and organiser of a new system of production that was able to overcome the historical downturn in the rate of profit that had emerged on the eve of World War I.

But what is the situation today? American imperialism may be the dominant global power, but it does not have a new regime of production capable of establishing a global economic equilibrium and a new expansionary phase of capitalist development. On the contrary, it seeks to counteract the impact of its economic decline through military means. And that signifies, notwithstanding our two authors, that inter-imperialist conflicts will deepen and intensify.

On the economic plane, the dominance of American finance is not an expression of strength, but of an historic crisis. Finance capital facilitates the accumulation of great wealth, but it is not engaged in the all-important—from the standpoint of the accumulation process in the capitalist economy as a whole—extraction of surplus value from the working class. Rather, it is engaged in the appropriation of surplus value extracted elsewhere. While finance capital is completely necessary for the expanded development of capitalism, it is, at the same time, parasitic.

If not America, can perhaps the industrialisation of China provide a new lease of life to the global capitalist order? After all, it could be argued that the massive reduction in the cost of labour resulting from the shifting of production to China, and of service operations to India, will boost the profit rate.

Let us consider what such a development would involve. For a start, it would require a massive growth in the Chinese economy. But even as this process gets underway, it has led to conflicts with the United States. China has already been designated a “strategic competitor”.

Furthermore, the industrialisation of China is disrupting class relations in all the major capitalist countries, where the working class is facing the consequences of economic globalisation. In the United States, for example, the massive wage cuts initiated by Delphi are an expression of the extreme pressure being exerted on wages and social conditions. This pressure is reflected in the drive to eliminate pension plans, where they still exist, in order to make American-based firms internationally competitive. In Europe, British Prime Minister Tony Blair has pointed to the necessity for a reform process—essentially the dismantling of social welfare measures—in order to remain competitive with China. And in Australia, Prime Minister John Howard has explained that one of the reasons for the recent sweeping changes to the industrial relations system was competition from China and India.

Then there is the situation in China itself. Tens of millions of people are being drawn into the international working class. At the present stage, to the extent that economic growth continues, there may well be illusions in the regime. That, however, can change rapidly as the process of industrialisation inevitably leads to all kinds of economic and political shocks. One only has to look to the turbulence that accompanied the industrialisation of Russia at the end of the nineteenth century—and the processes underway in China are developing on a far larger scale.

International relations are characterised by increased tensions. Not only is there the impact of China on the immediate region, but the relationship of China to other areas of the world, such as Latin America, the Middle East and Europe, where conflicts will, and already are, arising over raw materials, markets and political influence. China’s relationships with each of the major powers will exacerbate the conflicts among them. For example, despite its unconditional support for the Iraq war and Bush’s “war on terror” even the Howard government has warned Washington that it should not assume Australia will line up behind the US if a conflict were to develop with China over Taiwan.

As the whole of history demonstrates, the rise of a new industrial power disrupts the existing balance of power and fuels inter-imperialist conflicts and rivalries. At a certain point, this can lead to the eruption of war and the descent into barbarism. How is the working class to respond? It must initiate the task of reorganising the global economy on socialist foundations. Here we come to the crucial question of political perspective, which develops through a continuous analysis of every aspect of the world situation and its strategic implications. It is this that lies at the heart of the tasks facing the World Socialist Web Site in the coming period.

Our analysis has demonstrated that 35 years after the breakdown of the Bretton Woods system and the equilibrium established in the aftermath of World War II, world capitalism has not only been unable to establish a new equilibrium, its contradictions are creating the conditions for profound disequilibrium. The previous period of globalisation from 1870 to 1914 led to wars and revolution. The outcome of the present phase of globalisation will be no less explosive. It is precisely for this situation that we must prepare.

Concluded